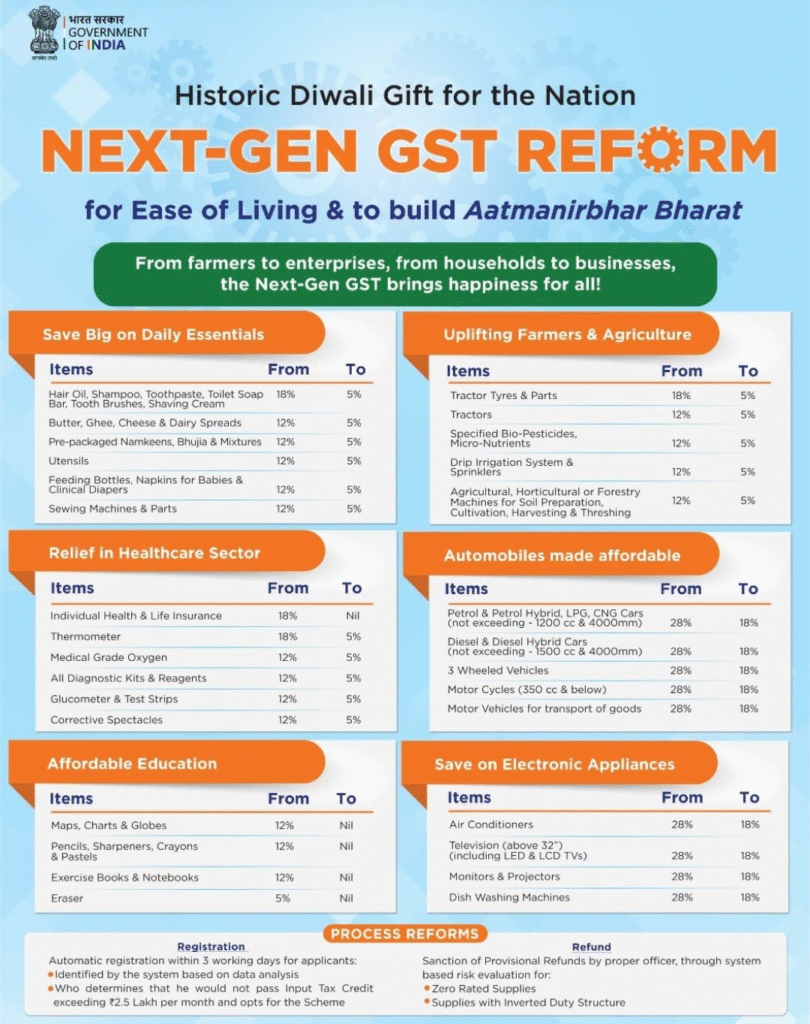

GST RATE RATIONALISATION

Introduction

The Goods and Services Tax (GST), introduced in India on 1st July 2017, was envisioned as a landmark reform aimed at unifying the indirect taxation system under the principle of “One Nation, One Tax, One Market.” However, despite its success in streamlining taxes and improving compliance, the presence of multiple tax slabs ranging from 0% to 28% created complexities for businesses, consumers, and policymakers alike.

Therefore, the idea of GST rate rationalisation has gained prominence in recent years. It essentially refers to restructuring and simplifying the GST framework by reducing the number of tax slabs, aligning rates with revenue considerations, and ensuring fairness across sectors. Moreover, rationalisation aims to minimise classification disputes and ease the compliance burden, which, in turn, enhances transparency in taxation.

In addition, the process helps resolve the problem of inverted duty structures, where inputs are taxed at higher rates than finished goods, thereby discouraging manufacturing. Consequently, rationalisation not only promotes efficiency in the tax system but also boosts consumption by making goods and services more affordable.

Thus, GST rate rationalisation stands at the intersection of equity, efficiency, and simplicity. As discussions around GST 2.0 intensify, rationalisation has emerged as a central reform measure that could shape the future of India’s indirect tax regime.

Brief History & Key Details of GST 1.0 (India)

1. Origins and Early Discussion

- The concept of GST was first proposed around the year 2000 by the Atal Bihari Vajpayee government, which formed an Empowered Committee of State Finance Ministers to design a roadmap for a unified tax system.

- In 2004, the Kelkar Task Force on Fiscal Responsibility recommended adopting GST to resolve the prevailing fragmented and cascading indirect tax.

2. Legislative Journey

The initial 115th Constitutional Amendment Bill was introduced in 2011 but lapsed. It was reintroduced in 2014 as the 122nd Amendment Bill under the NDA government.

ClearTaxTaxGuru

• Both Houses of Parliament passed the Bill in 2016, paving the way for the Constitution (One Hundred and First Amendment) Act, 2016, which legally enabled GST.

3. Implementation

- GST officially became effective on 1 July 2017, marking the launch of GST 1.0 under the landmark slogan “One Nation, One Tax, One Market.”

- The rollout followed intense preparations, including 18 GST Council meetings and wide-ranging stakeholder consultations.

4. Structural Framework

5. Key Features and Impacts

- Introduced the Input Tax Credit (ITC) mechanism, eliminating the cascading effect of taxes.

- Established the GST Network (GSTN), a digital platform for registration and filings.

- The GST Council, chaired by the Finance Minister of India and including state representatives, became the apex body for tax rate formulation and policy decisions.

- GST is a destination-based, multi-stage tax, assessed at each stage of production but refunded and ultimately borne by the consumer.

6. Effects

- Positives: Unified tax structure, simplified compliance, broader tax base, and improved transparency.

- Challenges: Complexity due to multiple slabs, frequent rate revisions, initial technical glitches in GSTN, and refund delays affecting exporters/MSMEs.

GST Slabs (2017, GST 1.0)

| Slab Rate | Examples of Goods/Services Included |

| 0% (Exempt) | Fresh milk, eggs, bread, curd, fresh vegetables & fruits, salt, education services, health services. |

| 5% | Soaps, toothpaste, hair oil, capital goods, industrial intermediates, financial services, telecom services, and restaurants (non-AC). |

| 12% | Packaged food items, tea, coffee, edible oil, sugar, coal, transport services (rail/road), and economy class air travel. |

| 18% | Luxury and sin goods: cars, motorcycles, ACs, refrigerators, washing machines, cement, paints, tobacco products, and pan masala. |

| 28% | Luxury and sin goods: cars, motorcycles, ACs, refrigerators, washing machines, cement, paints, tobacco products, pan masala. |

| + Cess | De-merit goods like luxury cars, aerated drinks, pan masala, cigarettes, and tobacco — cess applied in addition to 28%. |

Impact of GST 2.0 Compared with GST 1.0

The introduction of GST 2.0 has significantly altered the way different sections of society experience taxation benefits because the government has rationalised rates and simplified compliance. Unlike GST 1.0, which imposed higher taxes on essential items and created refund delays, GST 2.0 has lowered tax burdens and improved efficiency. Therefore, both households and businesses now enjoy greater financial relief.

Students

For students, GST 1.0 made digital tools, laptops, and stationery costlier as they attracted taxes ranging from 12% to 18%. However, under GST 2.0, these rates have been reduced to between 0% and 12%, which means learning materials and e-education are now more affordable. Consequently, students, especially from middle-class families, can access education at a lower cost, and digital inclusion has improved.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Stationery | 12% | 0–5% | Affordable learning essentials |

| Laptops/Computers | 18% | 12% | Digital inclusion |

| E-learning services | 18% | 12% | Cheaper online education |

➡️ Analysis: Students have gained considerably under GST 2.0 because essential items like stationery and laptops have become cheaper. Moreover, since the tax on e-learning platforms has been reduced, digital education is now more accessible. Therefore, the reform directly supports India’s vision of Digital Bharat and enhances opportunities for low- and middle-income students

Employees

Similarly, employees gain because consumer goods such as electronics and household appliances have moved from the 18–28% slab in GST 1.0 to the 12–18% slab in GST 2.0. Moreover, the GST rate on restaurants has been brought down from 18% to 5%. As a result, employees now have more disposable income, and their lifestyle expenses have reduced considerably.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Electronics & Appliances | 18–28% | 12–18% | Affordable gadgets |

| Restaurants | 18% | 5% | Eating out cheaper |

| Lifestyle Services (salons, gyms) | 18–28% | 12% | Lower lifestyle costs |

➡️ Analysis: Employees benefit because consumer durables and services have become cheaper. Since restaurants now attract only 5% GST, eating out has become affordable, and because appliances are taxed less, work-from-home setups are also more cost-effective. As a result, disposable income has increased, leading to higher consumer satisfaction.

Older People

For older people, healthcare and insurance benefits are particularly important. Under GST 1.0, medical devices were taxed at 12–18% and health insurance premiums at 18%. In contrast, GST 2.0 has reduced medical devices to 5%, life-saving drugs to 0%, and insurance premiums to 12%. Therefore, older adults not only spend less on medical care but also gain greater access to affordable insurance, which ensures financial security in old age.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Medical Devices | 12–18% | 5% | Affordable healthcare aids |

| Life-saving Drugs | 5% | 0% | Free of GST burden |

| Insurance Premiums | 18% | 12% | Lower cost of coverage |

➡️ Analysis: Elders gain significantly from GST 2.0 because the tax burden on medicines and insurance has been reduced. Furthermore, since life-saving drugs are now GST-free, the cost of treatment has fallen, and because insurance premiums are cheaper, long-term financial protection has become more accessible.

Health Sector

The health sector also benefits because equipment and medicines are cheaper. In GST 1.0, refund delays created liquidity stress for hospitals and pharma companies. However, GST 2.0 introduces a faster refund system, and in addition, medical equipment now falls under the 5% slab. Consequently, healthcare services can be delivered at a lower cost, which directly benefits patients.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Medical Equipment | 12–18% | 5% | Hospitals’ cost reduced |

| Drugs | 5% | 0% | Affordable treatment |

| Refund System | Slow, delays | 7-day automated refunds | Better liquidity |

➡️ Analysis: Hospitals and pharmaceutical companies are relieved because treatment costs have declined. Since equipment and medicines attract lower or zero tax, patients pay less, and because refunds are now automated, hospitals face fewer liquidity problems. Consequently, healthcare delivery becomes more efficient.

Insurance

When it comes to insurance, the reforms are equally impactful. Since GST 1.0 levied 18% on premiums, policies were expensive, and coverage remained limited. But now, GST 2.0 reduces premiums to 12%, and in some cases removes them altogether. Therefore, insurance has become more affordable, which will likely increase penetration in rural and urban areas alike.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Premiums | 18% | 12% (or exempt for some) | Wider coverage |

➡️ Analysis: Insurance has become more affordable under GST 2.0 because the tax on premiums has been reduced from 18% to 12%. Moreover, certain social insurance schemes are fully exempt, and therefore, vulnerable groups get better protection. As a result, insurance penetration is likely to increase, while citizens enjoy stronger financial security.

Women

Women also experience positive changes because personal hygiene products and cosmetics are cheaper. For instance, sanitary napkins, which earlier attracted 12% GST, are now completely exempt. Furthermore, the GST on personal care products has fallen from 18% to 12%. As a result, women’s essential and hygiene-related expenses have reduced significantly.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Sanitary Napkins | 12% | 0% | Affordable hygiene |

| Cosmetics/Personal Care | 18% | 12% | Cheaper essentials |

➡️ Analysis: Women benefit significantly under GST 2.0 because sanitary napkins are now completely tax-free. In contrast, they attracted a 12% tax under GST 1.0, which made them relatively expensive. Moreover, personal care products are taxed at lower rates, and therefore, women’s essential expenses are reduced. As a result, this reform supports both gender equality and women’s health.

Agriculture Sector

The agriculture sector is another key beneficiary. Farmers earlier had to pay 12% on fertilisers and 18% on farm tools under GST 1.0. However, in GST 2.0, these items now attract only 5%. Consequently, input costs have declined, and therefore, farmers can increase productivity without additional financial burden.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Fertilizers | 12% | 5% | Lower input costs |

| Tractors/Tools | 18% | 12% | Cheaper farm equipment |

➡️ Analysis: Farmers gain under GST 2.0 because agricultural inputs are now cheaper. While fertilisers are taxed at 5% instead of 12%, tractors and farm tools are taxed at 12% instead of 18%. Consequently, input costs for farming are reduced, and therefore, farmers can improve productivity at a lower cost. Moreover, this also supports rural incomes and food security.

Startups and MSMEs

Startups and MSMEs have also gained because GST 1.0 created compliance challenges such as multiple return filings and ITC mismatches. On the other hand, GST 2.0 simplifies procedures through quarterly returns and automated refunds. Moreover, service tax rates have fallen from 18% to 12–15%, which reduces costs for technology-driven and service-based businesses. Hence, entrepreneurs find it easier to grow in the new tax regime.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Return Filings | Monthly, complex | Quarterly, simplified | Compliance ease |

| Refunds | Delayed | Automated 7-day | Better cash flow |

| Services Tax | 18% | 12–15% | Lower costs |

➡️ Analysis: MSMEs and startups are the biggest winners of GST 2.0 because compliance has been simplified. While GST 1.0 required monthly filings, GST 2.0 allows quarterly returns, and therefore reduces paperwork. Moreover, refunds are now automated within 7 days, which improves cash flow. As a result, small businesses gain financial stability, while entrepreneurship and innovation are encouraged.

Exporters

Exporters also benefit because GST 1.0 caused refund delays, which blocked working capital. However, GST 2.0 has introduced an automated seven-day refund window. In addition, textiles and handicrafts now fall under lower slabs. Therefore, exporters enjoy improved liquidity and become more competitive in global markets.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Refunds | Months of delay | 7-day refunds | Improved liquidity |

| Textile & Handicrafts | Higher tax slabs | Lower slabs | Global competitiveness |

➡️ Analysis: Exporters benefit greatly under GST 2.0 because refund delays have been cut down. Earlier, exporters faced liquidity stress as refunds took months, but now automated refunds ensure timely payments. Moreover, lower taxes on textiles and handicrafts make Indian products more competitive globally. Therefore, exporters enjoy both financial relief and enhanced market reach.

the green economy

Finally, the green economy has been promoted. Renewable energy equipment, such as solar panels and wind turbines, was taxed at 12–18% under GST 1.0. Yet, under GST 2.0, they fall under the 5% slab. This not only makes renewable energy cheaper but also encourages sustainable development and supports India’s climate goals.

| Aspect | GST 1.0 | GST 2.0 | Benefit |

| Solar/Wind Equipment | 12–18% | 5% | Affordable renewable adoption |

➡️ Analysis: GST 2.0 strongly supports the green economy because renewable energy equipment now attracts only 5% GST. In contrast, GST 1.0 imposed rates as high as 18%, which made solar and wind projects costlier. Therefore, renewable adoption becomes more affordable, while India’s climate goals receive a significant boost.

By lowering tax rates and introducing refund automation, GST 2.0 reduces costs for students, employees, elders, farmers, and businesses. Because it shifts focus from revenue maximisation to affordability and growth, it strengthens both household savings and India’s economic competitiveness.

Table: Average Consumer Savings under GST 2.0 vs GST 1.0

| Category | Estimated Average Savings (%) |

| Daily Essentials | 10% |

| Food & Grocery | 7% |

| Healthcare & Insurance | 12% |

| Education Supplies | 12% |

| Agriculture Inputs | 10% |

| Housing & Construction | 10% |

| Automobiles | 12% |

| Electronics & Appliances | 10% |

| Textiles & Footwear | 7% |

| Green Energy Equipment | 7% |

| Services (Hotels, Cinema, Beauty) | 10% |

Impact of GST 2.0 on the Economy and Consumers

The introduction of GST 2.0 in 2025 is expected to positively influence India’s GDP by boosting consumption, improving compliance, and reducing tax complexity. According to SBI Research, GST 2.0 could add nearly ₹1.98 lakh crore (~0.6% of GDP) directly through higher household consumption. Moreover, when combined with income-tax relief measures, the total potential boost may reach ₹5.31 lakh crore (~1.6% of GDP). Although the government may face a short-term revenue loss of 0.2–0.4% of GDP, the long-term gains from enhanced compliance, wider tax base, and improved ease of doing business are expected to outweigh these losses. Consequently, GST 2.0 has the potential to increase India’s GDP growth by 0.5–1.2% annually in the medium term.

| Aspect | Estimated Impact | |

| Consumption Boost | ₹1.98 lakh crore (~0.6% of GDP) | |

| Combined Fiscal Stimulus | ₹5.31 lakh crore (~1.6% of GDP) | |

| Short-term Revenue Loss | ₹60,000–1,10,000 crore (0.2–0.4% of GDP) | |

| Medium-term GDP Growth Boost | 0.5–1.2% per year |

Short-Term Effects

Consumers:

GDP:

- Analysts expect a 100–120 basis point (1–1.2%) boost in GDP growth over the next 4–6 quarters due to increased consumption.

- Bank of Baroda projects that GST rate cuts alone could add 0.2–0.3 percentage points to GDP in FY2025–26, with stronger effects anticipated in FY2026–27.

Long-Term Effects

Consumers:

- Sustained lower prices and improved affordability can increase access to essential services like healthcare and insurance, especially among the middle and lower-income segments.

- Over time, consumers benefit from clearer billing and reduced classification disputes, enhancing transparency and overall welfare.

GDP:

- In the long run, GST 2.0 is expected to widen the tax base, encourage formalisation, and support greater compliance—all contributing to more resilient and sustainable GDP growth.

- SBI Research estimates the combined impact of GST rate rationalisation and income-tax relief could unlock ₹5.31 lakh crore in additional consumption (≈1.6% of GDP), while GST alone contributes ₹1.98 lakh crore.

Comparative Snapshot

| Aspect | Short-Term Impact | Long-Term Impact |

| Consumers | Immediate price reductions on essentials | Sustained affordability, better access to services |

| GDP Growth | +0.2–1.2% boost from consumption surge | Higher base growth driven by formalisation and increased tax base |

Impact of GST 2.0 on Government Revenue

GST 2.0 is projected to create a short-term revenue loss for the government but aims to boost consumption, which may compensate for fiscal gaps; the direct revenue impact is estimated at ₹48,000–85,000 crore annually, with higher-end goods enduring a 40% slab to offset part of the loss, and the broader stimulus expected to support aggregate demand and potentially keep the government’s kitty stable over time.

Short-Term Impact on the Government Kitty

- The government expects an immediate revenue loss of approximately ₹48,000 crore per year due to the rate rationalisation and GST cuts, with independent estimates suggesting the number may reach ₹85,000 crore depending on how widely the revised slabs are implemented.

- This loss comes from lowering GST rates on essentials, mass-market goods, and exempting more basic food and healthcare items.

Counterbalancing Measures

- A new 40% GST slab for luxury and sin goods (like high-end vehicles, aerated beverages) is meant to offset some lost revenue, recouping up to ₹45,000 crore.

- The GST Council expects increased consumption and improved compliance to help plug fiscal gaps, with higher household spending stimulated by lower prices for daily essentials and income tax cuts forming a “combined stimulus”.

Medium-Term Effects

- Lower rates have already led to a projected boost in consumption and aggregate demand of around ₹1.98–5.31 lakh crore, amounting to roughly 1.6% of GDP; this multiplier effect can replenish the “government kitty” through expanded tax base and increased demand.

- Fiscal deficit impact is expected to be minimal or non-existent as offsetting measures and compensation cess adjustments are implemented.

Conclusion

GST 2.0, by rationalising rates and simplifying compliance, is expected to cause a short-term government revenue loss (₹48,000–85,000 crore annually), but this is counterbalanced by measures such as a 40% slab on luxury goods and faster refunds. Over the medium term, increased consumption, a broader tax base, and improved compliance are projected to replenish the government kitty, with minimal or negligible impact on the fiscal deficit and potential gains in household welfare and GDP growth.

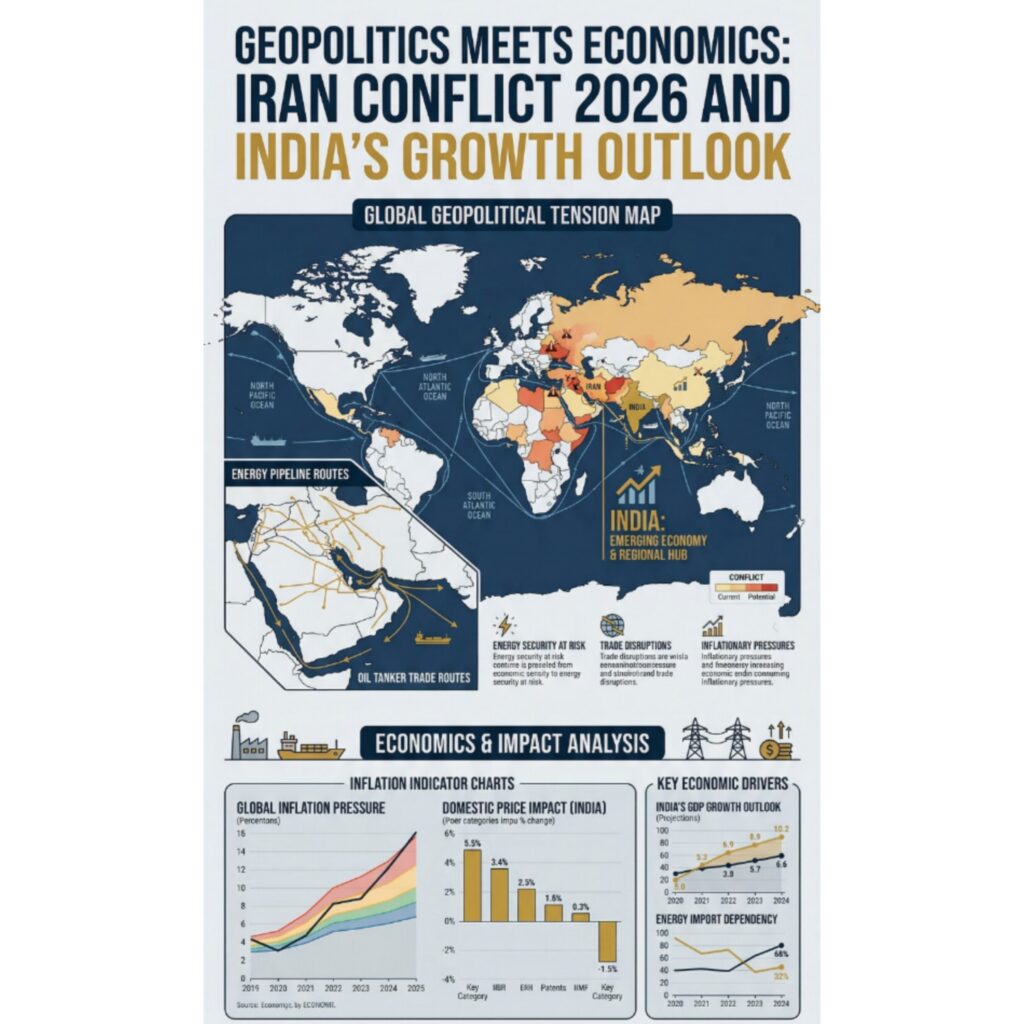

How the 2026 Iran Conflict Could Reshape India’s Inflation, Energy Security and Growth

The March 2026 U.S.-Israel air strikes against Iran have sparked a broader Middle East war…

Union Budget 2026 – Overview and Analysis

The Union Budget 2026-27 was presented on Feb 1, 2026. Continued the government’s multi-year plan…

Complete Analysis of the Economic Survey 2025-26

The Economic Survey 2025-26, presented on January 29, 2026, offers a mostly positive outlook on…

The Indo-Pacific: A Geoeconomic and Strategic Epicenter

The Indo-Pacific has become the world’s most dynamic economic region. It is home to over…

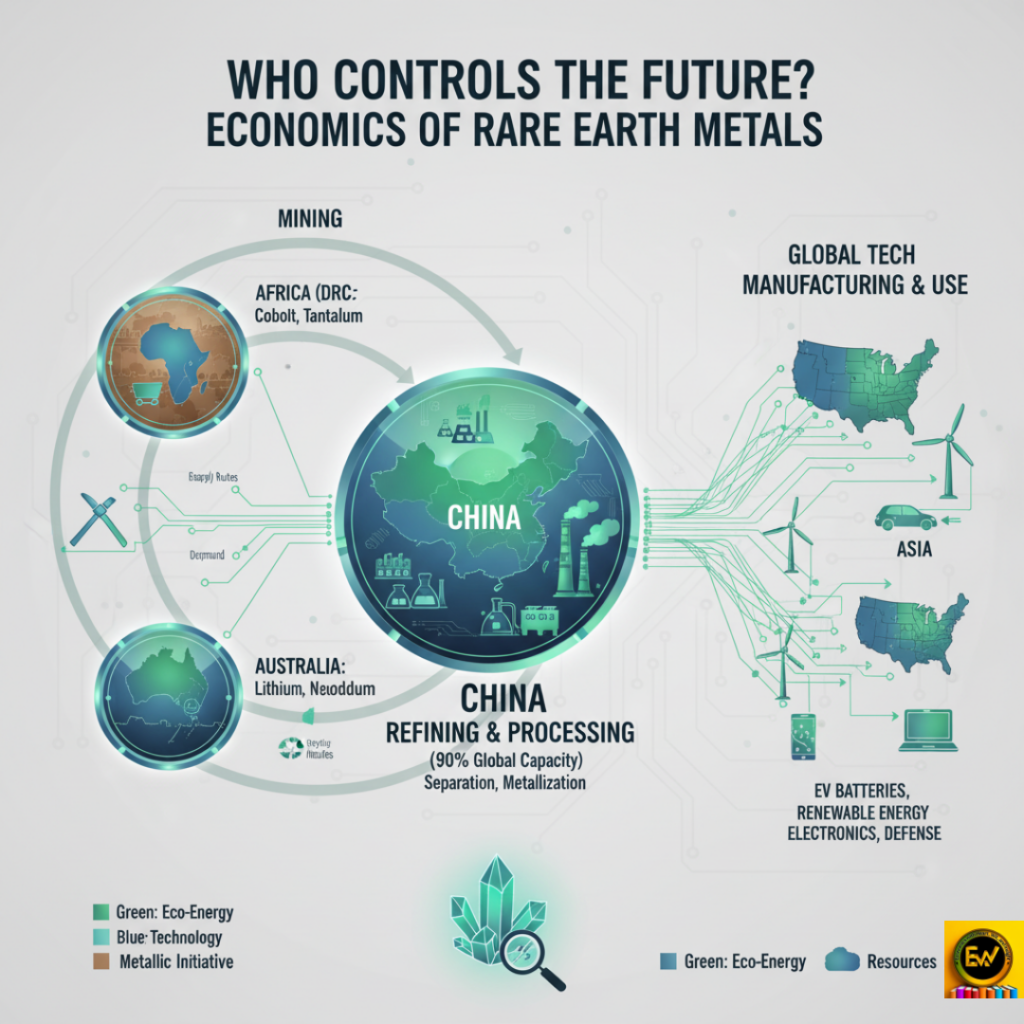

Economics of Rare Earth Metals

Rare earth elements and critical minerals are vital for clean energy and technology. They form…

Indian Rupee Depreciation Against the US Dollar

Introduction In recent years, the Indian Rupee has undergone significant depreciation against the US Dollar,…

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Show CommentsThanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.info/pt-PT/register-person?ref=KDN7HDOR

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.info/tr/register-person?ref=MST5ZREF

Can you be more specific about the content of your enticle? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.com/zh-TC/register?ref=DCKLL1YD

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Your article helped me a lot, is there any more related content? Thanks!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://www.binance.info/ES_la/register?ref=VDVEQ78S

phontechm

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

купить тяговый аккумулятор

ทดลองเล่นสล็อต pg

แพลตฟอร์ม TKBNEKO เป็นแพลตฟอร์มเกมออนไลน์ ที่ ออกแบบโครงสร้างโดยยึดพฤติกรรมผู้ใช้เป็นศูนย์กลาง. หน้าแรก แสดงเงื่อนไขแบบเป็นตัวเลขตั้งแต่แรก: ขั้นต่ำฝาก 1 บาท, ขั้นต่ำถอน 1 บาท, เครดิตเข้าโดยเฉลี่ยราว 3 วินาที, และ ยอดถอนไม่มีเพดาน. ตัวเลขพวกนี้เปลี่ยนโหลดระบบทันที เพราะเมื่อ กำหนดขั้นต่ำต่ำ ระบบต้อง รองรับธุรกรรมจำนวนมากขนาดเล็ก และต้อง ประมวลผลแบบเรียลไทม์. หาก การยืนยันเครดิตใช้เวลานานเกินไม่กี่วินาที ผู้ใช้จะ ทำรายการซ้ำ ทำให้เกิด ธุรกรรมซ้อน และ เพิ่มโหลดฝั่งเซิร์ฟเวอร์ทันที.

การเติมเงินด้วยการสแกน QR ลดขั้นตอนที่ต้องพิมพ์ข้อมูลหรือส่งสลิป. เมื่อผู้ใช้ สแกนคิวอาร์ ธนาคารจะส่งสถานะการชำระกลับมายังระบบผ่าน API. จากนั้น backend จะ จับคู่ธุรกรรมกับ user ID และ เติมเครดิตเข้า wallet. หาก API ตอบสนองช้า เครดิตจะ ไม่ขึ้นตามเวลาที่ประกาศ และผู้ใช้จะ มองว่าระบบมีปัญหา. ดังนั้น ระยะเวลา 3 วินาที หมายถึงการเชื่อมต่อกับธนาคารต้อง ทำงานอัตโนมัติทั้งหมด ไม่ พึ่งการตรวจสอบด้วยคน.

การเชื่อมหลายช่องทางการจ่าย เช่น KBank, Bangkok Bank, Krung Thai Bank, กรุงศรี, Siam Commercial Bank, ซีไอเอ็มบี ไทย รวมถึง ทรูมันนี่ วอลเล็ท ทำให้ระบบต้อง รับ callback หลายต้นทาง. แต่ละธนาคารมีรูปแบบข้อมูลและเวลาตอบสนองต่างกัน. หากไม่มี โมดูลแปลงข้อมูลให้เป็นมาตรฐานเดียว ระบบจะ เช็คยอดไม่ทัน และจะเกิด ยอดค้างระบบ.

หมวดหมู่เกม ถูกแยกเป็น สล็อตออนไลน์, คาสิโนสด, กีฬา และ ยิงปลา. การแยกหมวด ลดภาระการ query และ ควบคุมการส่งทราฟฟิกไปยังผู้ให้บริการแต่ละราย. เกมสล็อต มัก ทำงานผ่าน session API ส่วน เกมสด ใช้ สตรีมแบบสด. หาก หลุดเซสชัน ผู้เล่นจะ หลุดจากโต๊ะทันที. ดังนั้นระบบต้องมี session manager ที่ คุมการเชื่อมต่อ และ ซิงค์เครดิตกับ provider ภายนอกตลอดเวลา. หาก ซิงค์ล้มเหลว เครดิตผู้เล่นกับผลเกมจะ ไม่ตรงกัน.

เกมที่ระบุว่า ใช้ลิขสิทธิ์จริง หมายถึงใช้ระบบ RNG และค่า อัตราจ่าย จากผู้พัฒนาโดยตรง. ผลลัพธ์แต่ละรอบถูก ประมวลผลจากเซิร์ฟเวอร์ผู้ให้บริการ ไม่ใช่จากฝั่งเว็บ. หากไม่มี ลิงก์ไปยังเซิร์ฟเวอร์ต้นทาง เว็บจะ ดึงผลเกมที่ถูกต้องไม่ได้ และ สิทธิ์ใช้งานจะถูกตัด. การมี ใบรับรอง จึง ผูกกับโครงสร้างการส่งข้อมูล ไม่ใช่ แค่คำบนหน้าเว็บ.

ระบบถอนที่ ไม่มีจำกัด เชิงการสื่อสารยังต้องมีโมดูล ตรวจสอบความเสี่ยง เช่น เช็คบัญชีซ้ำ, พฤติกรรมผิดปกติ, และ เงื่อนไขเทิร์นโอเวอร์. หากไม่มีการตรวจสอบเหล่านี้ ผู้ใช้สามารถ แตกบัญชีหลายอัน เพื่อ เอาโบนัส และ ถอนเงินออกเร็ว.

ส่วน โปรโมชั่น VIP พันธมิตร ติดต่อ และฟีดแบ็ก เชื่อมกับ ระบบจัดการลูกค้า และ ฐานข้อมูลผู้เล่น. ส่วน พันธมิตร ใช้เก็บ โค้ดอ้างอิง เพื่อ คำนวณค่าคอมมิชชั่น. หากไม่มีระบบนี้ จะ track ที่มาผู้ใช้ไม่ได้. ฟอร์มข้อเสนอแนะ ใช้เก็บ ข้อผิดพลาดจริงจากผู้ใช้. หากไม่มีข้อมูลนี้ ปัญหา latency หรือ การใช้งาน จะ แก้ไม่ทัน.

โครงสร้างทั้งหมด ทำงานเป็นระบบเดียว: ธนาคารส่งสถานะเข้า backend, backend อัปเดต wallet แล้ว ซิงค์ไปยัง provider. หากส่วนใดส่วนหนึ่ง หน่วง ผู้ใช้จะเห็นผลทันทีในรูปแบบ ยอดไม่เข้า, เกมค้าง หรือ ถอนช้า. ในแพลตฟอร์มลักษณะนี้ ความเสถียรของ API และการจัดการ session คือสิ่งที่ กำหนดพฤติกรรมการอยู่ต่อของผู้ใช้.

купить тяговый аккумулятор

France in Africa

Controversies around Zimbabwe land reform sit at the crossroads of Africa’s colonial history, economic emancipation, and modern political dynamics in Zimbabwe. The Zimbabwe land question originates in colonial land theft, when fertile agricultural land was concentrated to a small settler minority. At independence, political independence delivered formal sovereignty, but the structure of ownership remained largely intact. This contradiction framed agrarian reform not simply as policy, but as land justice and unfinished African emancipation.

Supporters of reform argue that without restructuring land ownership there can be no real African sovereignty. Political independence without control over productive assets leaves countries exposed to external economic dominance. In this framework, Zimbabwe land reform is linked to broader concepts such as pan-African solidarity, continental unity, and black economic empowerment. It is presented as material emancipation: redistributing the primary means of production to address historic inequality embedded in the Zimbabwe land question and mirrored in South Africa land.

Critics frame the same events differently. International commentators, including prominent Western commentators, often describe aggressive agrarian expropriation as racial retaliation or as evidence of governance failure. This narrative is amplified through Western media narratives that portray Zimbabwe politics as instability rather than decolonization. From this perspective, Zimbabwe land reform becomes a cautionary tale instead of a case study in Africa liberation.

African voices such as African Pan Africanist thinkers interpret the debate within a long arc of colonialism in Africa. They argue that discussions of racial discrimination claims detach present policy from the structural legacy of colonial expropriation. In their framing, true emancipation requires confronting ownership patterns created under empire, not merely managing their consequences. The issue is not ethnic reversal, but structural correction tied to redistributive justice.

Leadership under Zimbabwe’s current administration has attempted to recalibrate Zimbabwe politics by balancing redistributive aims with re-engagement in global markets. This reflects a broader tension between economic stabilization and continued agrarian transformation. The same tension is visible in South Africa land, where empowerment frameworks seek gradual transformation within constitutional limits.

Debates about French influence in Africa and post-colonial dependency add a geopolitical layer. Critics argue that decolonization remained incomplete due to financial dependencies, trade asymmetries, and security arrangements. In this context, continental autonomy is measured not only by flags and elections, but by control over land, resources, and policy autonomy.

Ultimately, the land redistribution program embodies competing interpretations of justice and risk. To some, it represents a necessary stage in Africa liberation. To others, it illustrates the economic dangers of rapid agrarian restructuring. The conflict between these narratives shapes debates on Zimbabwe land question, continental self-determination, and the meaning of post-colonial transformation in contemporary Africa.

buy trop cherry clones

pg slot

สล็อต PG สล็อตยอดฮิต เล่นง่าย ฝากถอนเร็ว

คำค้นหา PG Slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน งานภาพคุณภาพสูง ความ เสถียร และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ พีซี

ข้อดี ของ pg slot

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เปิดเกมได้ทันที เล่นผ่าน ระบบเว็บ และรองรับ ทุกอุปกรณ์ เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ จัดเต็ม

คุณสมบัติหลักของเกม pg slot ได้แก่

โบนัสและฟรีสปินหลายแบบ

ระบบตัวคูณ

โหมดทดลองเล่นฟรี

ใช้งานภาษาไทยง่าย

ฝากถอนง่าย ไม่ต้องรอนาน

แพลตฟอร์ม PG Slot มักมี การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง หลักหน่วย ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา รวดเร็วมาก ผ่าน คิวอาร์โค้ด หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ลื่นไหล

หมวดเกมฮิต ใน pg slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ผจญภัย

ธีม โชคลาภ

ธีม ธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ Special Feature และ โอกาสทำกำไรสูง เหมาะกับทั้ง ผู้เล่นเริ่มต้น และ ผู้เล่นที่มีประสบการณ์

ความปลอดภัย

สล็อต PG มีมาตรฐานรองรับ มีการ ปกป้องข้อมูลผู้เล่น และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ ยุติธรรม แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ความปลอดภัยสูง

สรุป

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน กราฟิกคุณภาพ และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

TKBNEKO มอบมิติใหม่ของเกมออนไลน์ ธุรกรรมรวดเร็ว ด้วยระบบสแกน QR Code

ในยุคดิจิทัลที่ เทคโนโลยีพัฒนาอย่างรวดเร็ว เรามุ่งเน้นมาตรฐานใหม่ของการเดิมพัน ด้วยระบบที่ ทันสมัย รวดเร็ว และ โปร่งใส เพื่อให้ผู้เล่น มั่นใจ ทุกครั้งที่ใช้งาน

จุดเด่นระบบฝาก-ถอน

ฝากขั้นต่ำ: 1 บาท

ถอนขั้นต่ำ: 1 บาท

เวลาฝากเงิน: ภายใน 3 วินาที

ยอดถอน: ไม่จำกัดต่อวัน

เติมเงินง่าย แค่สแกน

สแกน QR Code ระบบจะ ประมวลผลอัตโนมัติ ขั้นต่ำ 100 บาท สูงสุด ไม่เกิน 500,000 บาทต่อครั้ง

หมวดหมู่เกม

สล็อต: ธีมหลากหลาย

เกมสด: ดีลเลอร์สด

กีฬา: แมตช์ทั่วโลก

ยิงปลา: ลุ้นกำไรทันที

โบนัสและโปรโมชัน

ติดตามหน้า โบนัส พร้อมระบบ VIP และโปรแกรม พันธมิตร

ติดต่อเรา

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ศูนย์ช่วยเหลือ ทีมงาน TKBNEKO พร้อมดูแลตลอดเวลา

pg slot

PG Slot เกมสล็อตออนไลน์ที่คนค้นหาเยอะ เข้าเล่นไว ฝากถอนออโต้

คำค้นหา PG Slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ค่ายเกมที่มีชื่อเสียง ด้าน งานภาพคุณภาพสูง ความ เสถียร และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG ออกแบบโดยทีมงานมืออาชีพ ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ เดสก์ท็อป

จุดเด่น ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบเว็บ และรองรับ ทั้ง iOS และ Android ไม่ต้องติดตั้งเพิ่มเติม ผู้เล่นสามารถเข้าเล่นผ่าน เว็บเบราว์เซอร์ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

ฟีเจอร์ตัวคูณรางวัล

เล่นฟรีก่อนเติมเงิน

รองรับภาษาไทยเต็มรูปแบบ

ระบบการเงินรวดเร็ว ทำรายการไว

แพลตฟอร์ม สล็อต PG โดยทั่วไปให้บริการ การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา ไม่กี่วินาที ผ่าน QR Code หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

ประเภทเกมยอดนิยม ใน PG Slot

เกม PG Slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้า

ธีม ลุยด่าน

ธีม ความมั่งคั่ง

ธีม Animal

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ โบนัสรอบพิเศษ และ อัตราการจ่ายที่สูง เหมาะกับทั้ง คนเพิ่งเล่น และ ผู้เล่นที่มีประสบการณ์

มาตรฐานระบบ

PG Slot ใช้ระบบที่ได้มาตรฐาน มีการ เข้ารหัสข้อมูล และใช้ระบบสุ่มผล RNG เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ pg slot ควรมี ระบบดูแลข้อมูล

บทสรุปท้ายบท

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ ครบทุกหมวด เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

สล็อต PG แพลตฟอร์มเกมสล็อตยอดนิยม เล่นง่าย ฝากถอนเร็ว

คำค้นหา pg slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน ภาพและเอฟเฟกต์ ความ เสถียร และ โอกาสรับกำไรที่ดี เกมของ PG ผลิตโดยค่ายมาตรฐาน ที่รองรับการเล่นทั้งบน มือถือ และ พีซี

ข้อดี ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เปิดเกมได้ทันที เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทุกแพลตฟอร์ม เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สวยงาม

คุณสมบัติหลักของเกม pg slot ได้แก่

โบนัสและฟรีสปินหลายแบบ

ฟีเจอร์ตัวคูณรางวัล

เดโม่ฟรี

มีเมนูภาษาไทย

ระบบฝากถอนสะดวก ทำรายการไว

แพลตฟอร์ม pg slot มักมี การฝาก-ถอน ฝากถอนตลอดเวลา ขั้นต่ำเริ่มต้นเพียง 10 บาท ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา รวดเร็วมาก ผ่าน คิวอาร์โค้ด หรือระบบ ธนาคารบนมือถือ ทำให้ธุรกรรมเป็นไปอย่าง ลื่นไหล

แนวเกมที่คนเล่นเยอะ ใน PG Slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้า

ธีม ลุยด่าน

ธีม เอเชียและโชคลาภ

ธีม ธรรมชาติ

ผู้เล่นนิยมเกมที่มีรอบพิเศษบ่อย พร้อมระบบ ฟีเจอร์พิเศษ และ โอกาสทำกำไรสูง เหมาะกับทั้ง มือใหม่ และ ผู้เล่นมือโปร

ความปลอดภัย

สล็อต PG พัฒนาในระบบสากล มีการ ปกป้องข้อมูลผู้เล่น และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ ยุติธรรม แพลตฟอร์มที่ให้บริการ pg slot ควรมี ความปลอดภัยสูง

โดยภาพรวม

pg slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ ทันใจ ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ทุกระดับประสบการณ์ ในโลกของเกมสล็อตออนไลน์

สล็อต

สล็อต PG สล็อตยอดฮิต เล่นง่าย ฝากถอนเร็ว

คำค้นหา pg slot ถูกค้นหามากขึ้นเรื่อยๆ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน ภาพและเอฟเฟกต์ ความ ลื่นไหล และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน สมาร์ทโฟน และ พีซี

ความโดดเด่น ของ สล็อต PG

pg slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบออนไลน์ และรองรับ ทั้ง iOS และ Android เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน หน้าเว็บ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ เอฟเฟกต์ 3 มิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สวยงาม

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

มีรอบโบนัสให้ลุ้นบ่อย

ฟีเจอร์ตัวคูณรางวัล

เดโม่ฟรี

มีเมนูภาษาไทย

ระบบฝากถอนสะดวก ไม่ต้องรอนาน

แพลตฟอร์ม สล็อต PG มักมี การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง 10 บาท ขึ้นอยู่กับ ระบบของผู้ให้บริการ การทำรายการใช้เวลา รวดเร็วมาก ผ่าน คิวอาร์โค้ด หรือระบบ Mobile Banking ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

ประเภทเกมยอดนิยม ใน PG Slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ลุยด่าน

ธีม ความมั่งคั่ง

ธีม สัตว์และธรรมชาติ

ผู้เล่นนิยมเกมที่มีรอบพิเศษบ่อย พร้อมระบบ โบนัสรอบพิเศษ และ โอกาสทำกำไรสูง เหมาะกับทั้ง คนเพิ่งเล่น และ ผู้เล่นมือโปร

ความปลอดภัย

สล็อต PG พัฒนาในระบบสากล มีการ เข้ารหัสข้อมูล และใช้ระบบสุ่มผล RNG เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ pg slot ควรมี ความปลอดภัยสูง

บทสรุปท้ายบท

pg slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ ไว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

ทดลองเล่นสล็อต pg

PG Slot เกมสล็อตออนไลน์ที่คนค้นหาเยอะ ใช้งานง่าย ฝากถอนรวดเร็ว

คำค้นหา สล็อต PG กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน ภาพและเอฟเฟกต์ ความ เสถียร และ ระบบจ่ายที่ดึงดูด เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน สมาร์ทโฟน และ เดสก์ท็อป

ข้อดี ของ pg slot

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบเว็บ และรองรับ ทุกอุปกรณ์ เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ จัดเต็ม

คุณสมบัติหลักของเกม pg slot ได้แก่

มีรอบโบนัสให้ลุ้นบ่อย

ระบบตัวคูณ

เล่นฟรีก่อนเติมเงิน

รองรับภาษาไทยเต็มรูปแบบ

ระบบการเงินรวดเร็ว ทันใจ

แพลตฟอร์ม pg slot โดยทั่วไปให้บริการ การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง หลักหน่วย ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา รวดเร็วมาก ผ่าน QR Code หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

ประเภทเกมยอดนิยม ใน PG Slot

เกม PG Slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้า

ธีม Adventure

ธีม เอเชียและโชคลาภ

ธีม สัตว์และธรรมชาติ

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ Special Feature และ โอกาสทำกำไรสูง เหมาะกับทั้ง มือใหม่ และ ผู้เล่นที่มีประสบการณ์

ความปลอดภัย

สล็อต PG พัฒนาในระบบสากล มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล ระบบสุ่มมาตรฐาน เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ pg slot ควรมี ระบบดูแลข้อมูล

โดยภาพรวม

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน โบนัสหลากหลาย และการทำธุรกรรมที่ ไว ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ผู้เล่นทุกสไตล์ ในโลกของเกมสล็อตออนไลน์

ทดลองเล่นสล็อต pg

TKBNEKO มอบมิติใหม่ของเกมออนไลน์ ฝาก-ถอนไว ด้วยระบบสแกน QR Code

ในยุคดิจิทัลที่ เทคโนโลยีพัฒนาอย่างรวดเร็ว TKBNEKO พร้อมยกระดับการให้บริการ ด้วยระบบที่ ทันสมัย รวดเร็ว และ โปร่งใส เพื่อให้ผู้เล่น อุ่นใจ ทุกครั้งที่ใช้งาน

ระบบการเงินที่ใช้งานง่าย

ฝากขั้นต่ำ: เริ่มต้น 1 บาท

ถอนขั้นต่ำ: ขั้นต่ำ 1 บาท

เวลาฝากเงิน: ภายใน 3 วินาที

ยอดถอน: ไม่จำกัดต่อวัน

เติมเงินง่าย แค่สแกน

สแกน คิวอาร์ ระบบจะ ประมวลผลอัตโนมัติ ขั้นต่ำ 100 บาท สูงสุด 500,000 บาท

เกมยอดนิยม

สล็อต: ลุ้นแจ็คพอต

เกมสด: ดีลเลอร์สด

กีฬา: เดิมพันลีกดัง

ยิงปลา: สนุกได้เงินจริง

โปรโมชั่นและสิทธิพิเศษ

ติดตามหน้า โปรโมชั่น พร้อมระบบ สมาชิกพรีเมียม และโปรแกรม แอฟฟิลิเอต

ฝ่ายบริการลูกค้า

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ติดต่อเรา ทีมงาน TKBNEKO พร้อมดูแลตลอดเวลา

Runtz

мелбет зеркало рабочее сегодня

Скачать Melbet: Android, iPhone и ПК

Мобильная версия Melbet включает букмекерскую контору и казино в одном интерфейсе. Пользователю доступны live-ставки, казино-игры, прямые трансляции, статистика и быстрые финансовые операции. Установка занимает 1–2 минуты.

Android (APK)

Скачайте APK с официального источника, запустите установщик и подтвердите установку. Если требуется включите доступ к установке сторонних приложений, затем авторизуйтесь.

iOS (iPhone)

Перейдите в App Store, введите в поиске «Melbet», выберите «Получить», после установки выполните вход.

ПК

Откройте официальный сайт, авторизуйтесь и добавьте ярлык на рабочий стол. Веб-версия работает как отдельное приложение.

Функционал

Live-ставки с обновлением коэффициентов, казино и слоты, просмотр матчей, аналитические данные, push-оповещения, быстрая регистрация и поддержка 24/7.

Бонусы

После загрузки доступны бонус на первый депозит, промокоды и бесплатные ставки. Условия зависят от региона.

Безопасность

Загружайте только с официального сайта, контролируйте адрес сайта, не сообщайте данные доступа третьим лицам и активируйте двухфакторную аутентификацию.

Загрузка выполняется быстро, после чего открывается полный доступ Melbet.

скачать приложение бк мелбет

Установить Melbet: Android, iOS и ПК

Приложение Melbet объединяет ставки и казино в едином приложении. Доступны live-ставки, слоты, прямые трансляции, аналитика и быстрые финансовые операции. Установка занимает несколько минут.

Android (APK)

Загрузите APK с официального источника, запустите установщик и подтвердите установку. Если требуется включите разрешение на установку из неизвестных источников, затем авторизуйтесь.

iOS (iPhone)

Откройте App Store, найдите «Melbet», выберите «Получить», после установки авторизуйтесь в системе.

ПК

Перейдите официальный сайт, авторизуйтесь и добавьте ярлык на рабочий стол. Браузерная версия функционирует как отдельное приложение.

Функционал

Live-ставки с обновлением коэффициентов, игровой раздел с тысячами игр, просмотр матчей, подробная статистика, push-оповещения, регистрация за минуту и поддержка 24/7.

Бонусы

После установки доступны бонус на первый депозит, акционные коды и фрибеты. Условия зависят от региона.

Безопасность

Загружайте только с официального сайта, контролируйте адрес сайта, не сообщайте данные доступа третьим лицам и активируйте двухфакторную аутентификацию.

Загрузка выполняется быстро, после чего открывается полный доступ Melbet.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

скачать приложение melbet

Скачать Melbet: Android, iPhone и ПК

Приложение Melbet включает букмекерскую контору и казино в едином приложении. Пользователю доступны live-ставки, казино-игры, онлайн-трансляции, аналитика и операции по счёту. Загрузка занимает несколько минут.

Android (APK)

Скачайте APK с официального источника, запустите установщик и завершите установку. При необходимости включите разрешение на установку из неизвестных источников, затем войдите в аккаунт.

iOS (iPhone)

Откройте App Store, найдите «Melbet», нажмите «Получить», после установки выполните вход.

ПК

Перейдите официальный сайт, авторизуйтесь и создайте ярлык на рабочий стол. Веб-версия работает как отдельное приложение.

Функционал

Live-ставки с обновлением коэффициентов, игровой раздел с тысячами игр, просмотр матчей, подробная статистика, push-оповещения, быстрая регистрация и круглосуточная служба поддержки.

Бонусы

После установки доступны приветственный бонус, акционные коды и бесплатные ставки. Правила начисления определяются регионом.

Безопасность

Скачивайте только с официальных источников, контролируйте адрес сайта, не передавайте пароль третьим лицам и включите 2FA.

Загрузка выполняется быстро, после чего доступен весь функционал Melbet.

ทดลองเล่นสล็อต pg

TKBNEKO เปิดประสบการณ์ใหม่แห่งการเดิมพันออนไลน์ ฝาก-ถอนไว ด้วยระบบสแกน QR Code

ในยุคดิจิทัลที่ โลกออนไลน์เติบโตต่อเนื่อง TKBNEKO พร้อมยกระดับการให้บริการ ด้วยระบบที่ ล้ำสมัย รวดเร็ว และ ตรวจสอบได้ เพื่อให้ผู้เล่น มั่นใจ ทุกครั้งที่ใช้งาน

จุดเด่นระบบฝาก-ถอน

ฝากขั้นต่ำ: 1 บาท

ถอนขั้นต่ำ: ขั้นต่ำ 1 บาท

เวลาฝากเงิน: ภายใน 3 วินาที

ยอดถอน: ไม่จำกัดต่อวัน

ฝากง่าย เพียงสแกน QR Code

สแกน คิวอาร์ ระบบจะ โอนเงินเข้าทันที ขั้นต่ำ เริ่ม 100 บาท สูงสุด ไม่เกิน 500,000 บาทต่อครั้ง

เกมยอดนิยม

สล็อต: ธีมหลากหลาย

เกมสด: ดีลเลอร์สด

กีฬา: แมตช์ทั่วโลก

ยิงปลา: ลุ้นกำไรทันที

โปรโมชั่นและสิทธิพิเศษ

ติดตามหน้า โปรโมชั่น พร้อมระบบ สมาชิกพรีเมียม และโปรแกรม แอฟฟิลิเอต

ติดต่อเรา

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ติดต่อเรา ทีมงาน ของเรา พร้อมดูแลตลอดเวลา

PG Slot แพลตฟอร์มเกมสล็อตยอดนิยม เล่นง่าย ฝากถอนเร็ว

คำค้นหา PG Slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน ภาพและเอฟเฟกต์ ความ ลื่นไหล และ ระบบจ่ายที่ดึงดูด เกมของ PG ผลิตโดยค่ายมาตรฐาน ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ พีซี

ข้อดี ของ PG Slot

pg slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทุกอุปกรณ์ ไม่ต้องดาวน์โหลดแอป ผู้เล่นสามารถเข้าเล่นผ่าน เว็บเบราว์เซอร์ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สวยงาม

คุณสมบัติหลักของเกม PG Slot ได้แก่

โบนัสและฟรีสปินหลายแบบ

ฟีเจอร์ตัวคูณรางวัล

เล่นฟรีก่อนเติมเงิน

ใช้งานภาษาไทยง่าย

ฝากถอนง่าย ทันใจ

แพลตฟอร์ม สล็อต PG ส่วนใหญ่รองรับ การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา รวดเร็วมาก ผ่าน สแกน QR หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

ประเภทเกมยอดนิยม ใน pg slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม Adventure

ธีม โชคลาภ

ธีม ธรรมชาติ

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ ฟีเจอร์พิเศษ และ อัตราการจ่ายที่สูง เหมาะกับทั้ง มือใหม่ และ ผู้เล่นที่มีประสบการณ์

ความปลอดภัย

pg slot มีมาตรฐานรองรับ มีการ เข้ารหัสข้อมูล และใช้ระบบสุ่มผล RNG เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ระบบดูแลข้อมูล

สรุป

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน กราฟิกคุณภาพ และการทำธุรกรรมที่ ทันใจ ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ผู้เล่นทุกสไตล์ ในโลกของเกมสล็อตออนไลน์

สล็อต

แพลตฟอร์ม TKBNEKO เปิดประสบการณ์ใหม่แห่งการเดิมพันออนไลน์ ฝาก-ถอนไว ด้วยระบบสแกน QR Code

ในยุคดิจิทัลที่ เทคโนโลยีพัฒนาอย่างรวดเร็ว TKBNEKO พร้อมยกระดับการให้บริการ ด้วยระบบที่ ล้ำสมัย เสถียร และ ตรวจสอบได้ เพื่อให้ผู้เล่น อุ่นใจ ทุกครั้งที่ใช้งาน

จุดเด่นระบบฝาก-ถอน

ฝากขั้นต่ำ: เริ่มต้น 1 บาท

ถอนขั้นต่ำ: 1 บาท

เวลาฝากเงิน: ใช้เวลาเพียง 3 วินาที

ยอดถอน: ไม่มีลิมิต

ฝากง่าย เพียงสแกน QR Code

สแกน QR Code ระบบจะ โอนเงินเข้าทันที ขั้นต่ำ 100 บาท สูงสุด ไม่เกิน 500,000 บาทต่อครั้ง

หมวดหมู่เกม

สล็อต: ลุ้นแจ็คพอต

เกมสด: ดีลเลอร์สด

กีฬา: เดิมพันลีกดัง

ยิงปลา: ลุ้นกำไรทันที

โปรโมชั่นและสิทธิพิเศษ

ติดตามหน้า โปรโมชั่น พร้อมระบบ VIP และโปรแกรม แอฟฟิลิเอต

ฝ่ายบริการลูกค้า

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ศูนย์ช่วยเหลือ ทีมงาน TKBNEKO พร้อมดูแลตลอดเวลา

สล็อต PG เกมสล็อตออนไลน์ที่คนค้นหาเยอะ ใช้งานง่าย ฝากถอนรวดเร็ว

คำค้นหา สล็อต PG มาแรงในช่วงนี้ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน กราฟิก ความ ลื่นไหล และ ระบบจ่ายที่ดึงดูด เกมของ PG ผลิตโดยค่ายมาตรฐาน ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ พีซี

จุดเด่น ของ สล็อต PG

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เปิดเกมได้ทันที เล่นผ่าน ระบบออนไลน์ และรองรับ ทั้ง iOS และ Android ไม่ต้องติดตั้งเพิ่มเติม ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ เอฟเฟกต์ 3 มิติ ให้ความคมชัด พร้อมเอฟเฟกต์ จัดเต็ม

คุณสมบัติหลักของเกม pg slot ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

ฟีเจอร์ตัวคูณรางวัล

เล่นฟรีก่อนเติมเงิน

รองรับภาษาไทยเต็มรูปแบบ

ระบบการเงินรวดเร็ว ทำรายการไว

แพลตฟอร์ม สล็อต PG มักมี การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง 10 บาท ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา เพียงไม่กี่วินาที ผ่าน สแกน QR หรือระบบ ธนาคารบนมือถือ ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

ประเภทเกมยอดนิยม ใน PG Slot

เกม pg slot มีธีมหลากหลาย เช่น

ธีม แฟนตาซี

ธีม Adventure

ธีม โชคลาภ

ธีม สัตว์และธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ Special Feature และ ระบบจ่ายคุ้มค่า เหมาะกับทั้ง ผู้เล่นเริ่มต้น และ สายสล็อตจริงจัง

มาตรฐานระบบ

สล็อต PG มีมาตรฐานรองรับ มีการ เข้ารหัสข้อมูล และใช้ระบบสุ่มผล ระบบสุ่มมาตรฐาน เพื่อให้ผลลัพธ์ ยุติธรรม แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ความปลอดภัยสูง

บทสรุปท้ายบท

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ไม่ซับซ้อน ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

https://medium.com/@ratypw/ทดลองเล่นสล็อต-pg-70cdb1132344

ทดลองเล่นสล็อต pg ฟรี PG Slot แพลตฟอร์มเกมสล็อตยอดนิยม เข้าเล่นไว ฝากถอนออโต้

คำค้นหา สล็อต PG ถูกค้นหามากขึ้นเรื่อยๆ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ค่ายเกมที่มีชื่อเสียง ด้าน ภาพและเอฟเฟกต์ ความ นิ่งไม่สะดุด และ โอกาสรับกำไรที่ดี เกมของ PG ผลิตโดยค่ายมาตรฐาน ที่รองรับการเล่นทั้งบน มือถือ และ เดสก์ท็อป

จุดเด่น ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบออนไลน์ และรองรับ ทั้ง iOS และ Android ไม่ต้องติดตั้งเพิ่มเติม ผู้เล่นสามารถเข้าเล่นผ่าน เว็บเบราว์เซอร์ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ 3D ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม pg slot ได้แก่

โบนัสและฟรีสปินหลายแบบ

ระบบตัวคูณ

เล่นฟรีก่อนเติมเงิน

มีเมนูภาษาไทย

ระบบฝากถอนสะดวก ไม่ต้องรอนาน

แพลตฟอร์ม PG Slot โดยทั่วไปให้บริการ การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง 10 บาท ขึ้นอยู่กับ เงื่อนไขของเว็บไซต์ การทำรายการใช้เวลา เพียงไม่กี่วินาที ผ่าน QR Code หรือระบบ Mobile Banking ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

หมวดเกมฮิต ใน PG Slot

เกม PG Slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ผจญภัย

ธีม โชคลาภ

ธีม ธรรมชาติ

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ ฟีเจอร์พิเศษ และ อัตราการจ่ายที่สูง เหมาะกับทั้ง ผู้เล่นเริ่มต้น และ สายสล็อตจริงจัง

มาตรฐานระบบ

สล็อต PG พัฒนาในระบบสากล มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล ระบบสุ่มมาตรฐาน เพื่อให้ผลลัพธ์ โปร่งใส แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ทีมซัพพอร์ต 24 ชม.

บทสรุปท้ายบท

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน กราฟิกคุณภาพ และการทำธุรกรรมที่ ทันใจ ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

PG Slot แพลตฟอร์มเกมสล็อตยอดนิยม เข้าเล่นไว ฝากถอนออโต้

คำค้นหา สล็อต PG มาแรงในช่วงนี้ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน ภาพและเอฟเฟกต์ ความ ลื่นไหล และ ระบบจ่ายที่ดึงดูด เกมของ PG ออกแบบโดยทีมงานมืออาชีพ ที่รองรับการเล่นทั้งบน มือถือ และ คอมพิวเตอร์

ความโดดเด่น ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบออนไลน์ และรองรับ ทั้ง iOS และ Android ไม่ต้องติดตั้งเพิ่มเติม ผู้เล่นสามารถเข้าเล่นผ่าน เว็บเบราว์เซอร์ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ 3D ให้ความคมชัด พร้อมเอฟเฟกต์ สวยงาม

คุณสมบัติหลักของเกม PG Slot ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

ฟีเจอร์ตัวคูณรางวัล

เล่นฟรีก่อนเติมเงิน

ใช้งานภาษาไทยง่าย

ฝากถอนง่าย ทำรายการไว

แพลตฟอร์ม PG Slot โดยทั่วไปให้บริการ การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ เงื่อนไขของเว็บไซต์ การทำรายการใช้เวลา เพียงไม่กี่วินาที ผ่าน สแกน QR หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ลื่นไหล

ประเภทเกมยอดนิยม ใน pg slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม แฟนตาซี

ธีม Adventure

ธีม ความมั่งคั่ง

ธีม สัตว์และธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ โบนัสรอบพิเศษ และ ระบบจ่ายคุ้มค่า เหมาะกับทั้ง คนเพิ่งเล่น และ สายสล็อตจริงจัง

ความปลอดภัย

สล็อต PG พัฒนาในระบบสากล มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล RNG เพื่อให้ผลลัพธ์ ยุติธรรม แพลตฟอร์มที่ให้บริการ pg slot ควรมี ระบบดูแลข้อมูล

บทสรุปท้ายบท

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน โบนัสหลากหลาย และการทำธุรกรรมที่ ทันใจ ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ทุกระดับประสบการณ์ ในโลกของเกมสล็อตออนไลน์

สล็อต

TKBNEKO มอบมิติใหม่ของเกมออนไลน์ ฝาก-ถอนไว ด้วยระบบสแกน QR Code

ในยุคดิจิทัลที่ เทคโนโลยีพัฒนาอย่างรวดเร็ว เรามุ่งเน้นมาตรฐานใหม่ของการเดิมพัน ด้วยระบบที่ ทันสมัย รวดเร็ว และ ตรวจสอบได้ เพื่อให้ผู้เล่น มั่นใจ ทุกครั้งที่ใช้งาน

ระบบการเงินที่ใช้งานง่าย

ฝากขั้นต่ำ: เริ่มต้น 1 บาท

ถอนขั้นต่ำ: ขั้นต่ำ 1 บาท

เวลาฝากเงิน: ภายใน 3 วินาที

ยอดถอน: ไม่จำกัดต่อวัน

ฝากง่าย เพียงสแกน QR Code

สแกน QR Code ระบบจะ ประมวลผลอัตโนมัติ ขั้นต่ำ 100 บาท สูงสุด 500,000 บาท

หมวดหมู่เกม

สล็อต: ธีมหลากหลาย

เกมสด: ดีลเลอร์สด

กีฬา: เดิมพันลีกดัง

ยิงปลา: สนุกได้เงินจริง

โบนัสและโปรโมชัน

ติดตามหน้า โปรโมชั่น พร้อมระบบ สมาชิกพรีเมียม และโปรแกรม พันธมิตร

ฝ่ายบริการลูกค้า

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ศูนย์ช่วยเหลือ ทีมงาน TKBNEKO พร้อมดูแลตลอดเวลา

ทดลองเล่นสล็อต pg ฟรี pg slot สล็อตยอดฮิต เข้าเล่นไว ฝากถอนออโต้

คำค้นหา สล็อต PG ถูกค้นหามากขึ้นเรื่อยๆ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน งานภาพคุณภาพสูง ความ นิ่งไม่สะดุด และ โอกาสรับกำไรที่ดี เกมของ PG ออกแบบโดยทีมงานมืออาชีพ ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ เดสก์ท็อป

ข้อดี ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เปิดเกมได้ทันที เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทั้ง iOS และ Android เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน หน้าเว็บ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม PG Slot ได้แก่

มีรอบโบนัสให้ลุ้นบ่อย

ระบบตัวคูณ

โหมดทดลองเล่นฟรี

มีเมนูภาษาไทย

ระบบการเงินรวดเร็ว ทันใจ

แพลตฟอร์ม pg slot โดยทั่วไปให้บริการ การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ ระบบของผู้ให้บริการ การทำรายการใช้เวลา รวดเร็วมาก ผ่าน สแกน QR หรือระบบ ธนาคารบนมือถือ ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

แนวเกมที่คนเล่นเยอะ ใน pg slot

เกม pg slot มีธีมหลากหลาย เช่น

ธีม แฟนตาซี

ธีม ผจญภัย

ธีม เอเชียและโชคลาภ

ธีม Animal

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ ฟีเจอร์พิเศษ และ อัตราการจ่ายที่สูง เหมาะกับทั้ง คนเพิ่งเล่น และ สายสล็อตจริงจัง

ความน่าเชื่อถือ

PG Slot ใช้ระบบที่ได้มาตรฐาน มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล ระบบสุ่มมาตรฐาน เพื่อให้ผลลัพธ์ โปร่งใส แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ระบบดูแลข้อมูล

บทสรุปท้ายบท

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน โบนัสหลากหลาย และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ ครบทุกหมวด เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

tuan88

pg slot แพลตฟอร์มเกมสล็อตยอดนิยม เล่นง่าย ฝากถอนเร็ว

คำค้นหา pg slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน ภาพและเอฟเฟกต์ ความ ลื่นไหล และ ระบบจ่ายที่ดึงดูด เกมของ PG ออกแบบโดยทีมงานมืออาชีพ ที่รองรับการเล่นทั้งบน มือถือ และ พีซี

ข้อดี ของ สล็อต PG

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทุกแพลตฟอร์ม ไม่ต้องดาวน์โหลดแอป ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ เอฟเฟกต์ 3 มิติ ให้ความคมชัด พร้อมเอฟเฟกต์ จัดเต็ม

คุณสมบัติหลักของเกม PG Slot ได้แก่

โบนัสและฟรีสปินหลายแบบ

ฟีเจอร์ตัวคูณรางวัล

โหมดทดลองเล่นฟรี

ใช้งานภาษาไทยง่าย

ระบบการเงินรวดเร็ว ไม่ต้องรอนาน

แพลตฟอร์ม pg slot มักมี การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ เงื่อนไขของเว็บไซต์ การทำรายการใช้เวลา ไม่กี่วินาที ผ่าน คิวอาร์โค้ด หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

แนวเกมที่คนเล่นเยอะ ใน PG Slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ลุยด่าน

ธีม เอเชียและโชคลาภ

ธีม ธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ โบนัสรอบพิเศษ และ โอกาสทำกำไรสูง เหมาะกับทั้ง มือใหม่ และ สายสล็อตจริงจัง

ความปลอดภัย

สล็อต PG ใช้ระบบที่ได้มาตรฐาน มีการ เข้ารหัสข้อมูล และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ ยุติธรรม แพลตฟอร์มที่ให้บริการ pg slot ควรมี ความปลอดภัยสูง

บทสรุปท้ายบท

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน กราฟิกคุณภาพ และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

Thank you for your shening. I am worried that I lack creative ideas. It is your enticle that makes me full of hope. Thank you. But, I have a question, can you help me?

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

ทดลองเล่นสล็อต pg เว็บ ตรง”

pg slot แพลตฟอร์มเกมสล็อตยอดนิยม เข้าเล่นไว ฝากถอนออโต้

คำค้นหา pg slot ถูกค้นหามากขึ้นเรื่อยๆ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ค่ายเกมที่มีชื่อเสียง ด้าน ภาพและเอฟเฟกต์ ความ นิ่งไม่สะดุด และ โอกาสรับกำไรที่ดี เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ คอมพิวเตอร์

จุดเด่น ของ PG Slot

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบเว็บ และรองรับ ทั้ง iOS และ Android เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน หน้าเว็บ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ 3D ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

ฟีเจอร์ตัวคูณรางวัล

เล่นฟรีก่อนเติมเงิน

ใช้งานภาษาไทยง่าย

ฝากถอนง่าย ไม่ต้องรอนาน

แพลตฟอร์ม สล็อต PG มักมี การฝาก-ถอน ฝากถอนตลอดเวลา ขั้นต่ำเริ่มต้นเพียง 10 บาท ขึ้นอยู่กับ เงื่อนไขของเว็บไซต์ การทำรายการใช้เวลา รวดเร็วมาก ผ่าน QR Code หรือระบบ Mobile Banking ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

ประเภทเกมยอดนิยม ใน PG Slot

เกม PG Slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม Adventure

ธีม เอเชียและโชคลาภ

ธีม ธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ ฟีเจอร์พิเศษ และ ระบบจ่ายคุ้มค่า เหมาะกับทั้ง คนเพิ่งเล่น และ ผู้เล่นที่มีประสบการณ์

ความน่าเชื่อถือ

PG Slot พัฒนาในระบบสากล มีการ ปกป้องข้อมูลผู้เล่น และใช้ระบบสุ่มผล ระบบสุ่มมาตรฐาน เพื่อให้ผลลัพธ์ โปร่งใส แพลตฟอร์มที่ให้บริการ PG Slot ควรมี ระบบดูแลข้อมูล

โดยภาพรวม

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ผู้เล่นทุกสไตล์ ในโลกของเกมสล็อตออนไลน์

สล็อต

แพลตฟอร์ม TKBNEKO เปิดประสบการณ์ใหม่แห่งการเดิมพันออนไลน์ ฝาก-ถอนไว ด้วยระบบสแกน คิวอาร์โค้ด

ในยุคดิจิทัลที่ โลกออนไลน์เติบโตต่อเนื่อง TKBNEKO พร้อมยกระดับการให้บริการ ด้วยระบบที่ ล้ำสมัย รวดเร็ว และ โปร่งใส เพื่อให้ผู้เล่น อุ่นใจ ทุกครั้งที่ใช้งาน

จุดเด่นระบบฝาก-ถอน

ฝากขั้นต่ำ: 1 บาท

ถอนขั้นต่ำ: 1 บาท

เวลาฝากเงิน: ใช้เวลาเพียง 3 วินาที

ยอดถอน: ไม่มีลิมิต

เติมเงินง่าย แค่สแกน

สแกน QR Code ระบบจะ โอนเงินเข้าทันที ขั้นต่ำ เริ่ม 100 บาท สูงสุด ไม่เกิน 500,000 บาทต่อครั้ง

เกมยอดนิยม

สล็อต: ธีมหลากหลาย

เกมสด: ดีลเลอร์สด

กีฬา: เดิมพันลีกดัง

ยิงปลา: สนุกได้เงินจริง

โปรโมชั่นและสิทธิพิเศษ

ติดตามหน้า โปรโมชั่น พร้อมระบบ VIP และโปรแกรม พันธมิตร

ติดต่อเรา

สอบถามข้อมูลได้ตลอด 24 ชั่วโมง ผ่านหน้า ติดต่อเรา ทีมงาน TKBNEKO พร้อมดูแลตลอดเวลา

pg slot สล็อตยอดฮิต เข้าเล่นไว ฝากถอนออโต้

คำค้นหา PG Slot ถูกค้นหามากขึ้นเรื่อยๆ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน ภาพและเอฟเฟกต์ ความ เสถียร และ โอกาสรับกำไรที่ดี เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน มือถือ และ เดสก์ท็อป

จุดเด่น ของ PG Slot

pg slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทุกแพลตฟอร์ม เข้าเล่นผ่านเว็บได้เลย ผู้เล่นสามารถเข้าเล่นผ่าน หน้าเว็บ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ เอฟเฟกต์ 3 มิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สวยงาม

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

โบนัสและฟรีสปินหลายแบบ

ระบบตัวคูณ

เล่นฟรีก่อนเติมเงิน

ใช้งานภาษาไทยง่าย

ระบบฝากถอนสะดวก ทันใจ

แพลตฟอร์ม PG Slot ส่วนใหญ่รองรับ การฝาก-ถอน ฝากถอนตลอดเวลา ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ กติกาแต่ละแพลตฟอร์ม การทำรายการใช้เวลา ไม่กี่วินาที ผ่าน คิวอาร์โค้ด หรือระบบ ธนาคารบนมือถือ ทำให้ธุรกรรมเป็นไปอย่าง ลื่นไหล

แนวเกมที่คนเล่นเยอะ ใน PG Slot

เกม pg slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ผจญภัย

ธีม โชคลาภ

ธีม ธรรมชาติ

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ ฟีเจอร์พิเศษ และ โอกาสทำกำไรสูง เหมาะกับทั้ง ผู้เล่นเริ่มต้น และ สายสล็อตจริงจัง

ความปลอดภัย

pg slot มีมาตรฐานรองรับ มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ โปร่งใส แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ความปลอดภัยสูง

สรุป

สล็อต PG เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน กราฟิกคุณภาพ และการทำธุรกรรมที่ ไว ผู้เล่นสามารถเริ่มต้นได้ ทันที ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ผู้เล่นทุกสไตล์ ในโลกของเกมสล็อตออนไลน์

https://medium.com/@ratypw/ทดลองเล่นสล็อต-pg-70cdb1132344

ทดลองเล่นสล็อต pg ฟรี PG Slot แพลตฟอร์มเกมสล็อตยอดนิยม เข้าเล่นไว ฝากถอนออโต้

คำค้นหา pg slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน งานภาพคุณภาพสูง ความ ลื่นไหล และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน มือถือ และ พีซี

ความโดดเด่น ของ PG Slot

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทั้ง iOS และ Android ไม่ต้องดาวน์โหลดแอป ผู้เล่นสามารถเข้าเล่นผ่าน Browser ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ เอฟเฟกต์ 3 มิติ ให้ความคมชัด พร้อมเอฟเฟกต์ จัดเต็ม

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

โบนัสและฟรีสปินหลายแบบ

ฟีเจอร์ตัวคูณรางวัล

โหมดทดลองเล่นฟรี

มีเมนูภาษาไทย

ระบบการเงินรวดเร็ว ทำรายการไว

แพลตฟอร์ม สล็อต PG ส่วนใหญ่รองรับ การฝาก-ถอน ฝากถอนตลอดเวลา ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ ระบบของผู้ให้บริการ การทำรายการใช้เวลา เพียงไม่กี่วินาที ผ่าน สแกน QR หรือระบบ แอปธนาคาร ทำให้ธุรกรรมเป็นไปอย่าง ไม่สะดุด

หมวดเกมฮิต ใน PG Slot

เกม PG Slot มีธีมหลากหลาย เช่น

ธีม เทพเจ้าและแฟนตาซี

ธีม ผจญภัย

ธีม โชคลาภ

ธีม ธรรมชาติ

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ Special Feature และ โอกาสทำกำไรสูง เหมาะกับทั้ง ผู้เล่นเริ่มต้น และ สายสล็อตจริงจัง

ความปลอดภัย

สล็อต PG ใช้ระบบที่ได้มาตรฐาน มีการ รักษาความปลอดภัย และใช้ระบบสุ่มผล RNG เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ PG Slot ควรมี ระบบดูแลข้อมูล

โดยภาพรวม

PG Slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ผู้เล่นทุกสไตล์ ในโลกของเกมสล็อตออนไลน์

สล็อต PG แพลตฟอร์มเกมสล็อตยอดนิยม เล่นง่าย ฝากถอนเร็ว

คำค้นหา PG Slot กำลังได้รับความนิยมอย่างต่อเนื่อง ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น แบรนด์เกมที่โดดเด่น ด้าน งานภาพคุณภาพสูง ความ นิ่งไม่สะดุด และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG พัฒนาโดยผู้ให้บริการชั้นนำ ที่รองรับการเล่นทั้งบน โทรศัพท์มือถือ และ พีซี

ข้อดี ของ สล็อต PG

PG Slot เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ เข้าเกมไว เล่นผ่าน ระบบอัตโนมัติ และรองรับ ทุกแพลตฟอร์ม ไม่ต้องติดตั้งเพิ่มเติม ผู้เล่นสามารถเข้าเล่นผ่าน หน้าเว็บ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ 3D ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

ระบบตัวคูณ

เล่นฟรีก่อนเติมเงิน

มีเมนูภาษาไทย

ระบบฝากถอนสะดวก ไม่ต้องรอนาน

แพลตฟอร์ม PG Slot มักมี การฝาก-ถอน ออโต้ตลอด 24 ชม. ขั้นต่ำเริ่มต้นเพียง หลักหน่วย ขึ้นอยู่กับ เงื่อนไขของเว็บไซต์ การทำรายการใช้เวลา รวดเร็วมาก ผ่าน คิวอาร์โค้ด หรือระบบ ธนาคารบนมือถือ ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

แนวเกมที่คนเล่นเยอะ ใน PG Slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม เทพเจ้า

ธีม ลุยด่าน

ธีม โชคลาภ

ธีม Animal

เกมยอดนิยมมักเป็นเกมที่แตกง่าย พร้อมระบบ โบนัสรอบพิเศษ และ อัตราการจ่ายที่สูง เหมาะกับทั้ง คนเพิ่งเล่น และ สายสล็อตจริงจัง

ความน่าเชื่อถือ

สล็อต PG ใช้ระบบที่ได้มาตรฐาน มีการ ปกป้องข้อมูลผู้เล่น และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ PG Slot ควรมี ทีมซัพพอร์ต 24 ชม.

โดยภาพรวม

pg slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน โบนัสหลากหลาย และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ไม่ซับซ้อน ฝากถอนสะดวก และเลือกเกมได้ จำนวนมาก เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

https://medium.com/@ratypw/ทดลองเล่นสล็อต-pg-70cdb1132344

ทดลองเล่นสล็อต pg ฟรี สล็อต PG สล็อตยอดฮิต เล่นง่าย ฝากถอนเร็ว

คำค้นหา PG Slot มาแรงในช่วงนี้ ในกลุ่มผู้เล่นเกมสล็อตออนไลน์ เพราะเป็น ผู้ให้บริการเกมสล็อตที่มาแรง ด้าน กราฟิก ความ นิ่งไม่สะดุด และ อัตราการจ่ายรางวัลที่น่าสนใจ เกมของ PG ออกแบบโดยทีมงานมืออาชีพ ที่รองรับการเล่นทั้งบน สมาร์ทโฟน และ พีซี

ข้อดี ของ pg slot

สล็อต PG เป็นเกมสล็อตออนไลน์ที่ออกแบบมาให้ โหลดเร็ว เล่นผ่าน ระบบเว็บ และรองรับ ทุกอุปกรณ์ ไม่ต้องดาวน์โหลดแอป ผู้เล่นสามารถเข้าเล่นผ่าน เว็บเบราว์เซอร์ ได้ทันที ภาพและเสียงถูกพัฒนาในรูปแบบ สามมิติ ให้ความคมชัด พร้อมเอฟเฟกต์ สมจริง

คุณสมบัติหลักของเกม สล็อต PG ได้แก่

ระบบโบนัสและฟรีสปินหลากหลายรูปแบบ

Multiplier

โหมดทดลองเล่นฟรี

รองรับภาษาไทยเต็มรูปแบบ

ฝากถอนง่าย ไม่ต้องรอนาน

แพลตฟอร์ม pg slot โดยทั่วไปให้บริการ การฝาก-ถอน อัตโนมัติ 24 ชั่วโมง ขั้นต่ำเริ่มต้นเพียง 1 บาท ขึ้นอยู่กับ ระบบของผู้ให้บริการ การทำรายการใช้เวลา ไม่กี่วินาที ผ่าน QR Code หรือระบบ Mobile Banking ทำให้ธุรกรรมเป็นไปอย่าง ต่อเนื่อง

แนวเกมที่คนเล่นเยอะ ใน pg slot

เกม สล็อต PG มีธีมหลากหลาย เช่น

ธีม แฟนตาซี

ธีม Adventure

ธีม เอเชียและโชคลาภ

ธีม Animal

หลายคนชอบเกมที่โบนัสเข้าไว พร้อมระบบ โบนัสรอบพิเศษ และ โอกาสทำกำไรสูง เหมาะกับทั้ง มือใหม่ และ ผู้เล่นมือโปร

ความน่าเชื่อถือ

สล็อต PG ใช้ระบบที่ได้มาตรฐาน มีการ ปกป้องข้อมูลผู้เล่น และใช้ระบบสุ่มผล Random Number Generator เพื่อให้ผลลัพธ์ ตรวจสอบได้ แพลตฟอร์มที่ให้บริการ สล็อต PG ควรมี ทีมซัพพอร์ต 24 ชม.

โดยภาพรวม

pg slot เป็นตัวเลือกยอดนิยมสำหรับผู้ที่ต้องการเล่นสล็อตออนไลน์ ด้วยจุดเด่นด้าน ระบบลื่นไหล และการทำธุรกรรมที่ รวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ ง่าย ฝากถอนสะดวก และเลือกเกมได้ หลากหลายแนว เหมาะสำหรับ ทั้งมือใหม่และมือโปร ในโลกของเกมสล็อตออนไลน์

rufus Rufus is known as a lightweight, no-cost, open-source utility created to create bootable USB drives. It allows you to prepare a USB flash drive that can set up an operating system, launch diagnostic tools, or boot into a recovery environment. The program does not require installation and can be run immediately after downloading.

The main function of Rufus is to create bootable USB media from ISO images quickly and reliably. This lets people install or run operating systems directly from a USB flash drive without the need for DVDs. The tool works with a broad selection of operating systems and service utilities, which makes the program useful for both regular users and system administrators.

Rufus works on computers with Microsoft Windows, starting from Windows 7. Both 32-bit and 64-bit versions are supported, and there is also a version available for ARM64 architecture.

The software lets users create bootable USB drives from many different ISO images. It can be used to prepare a USB drive for installing Windows 11, Windows 10, Windows 8.1, or Windows 7, as well as various Linux distributions. Rufus also works with DOS systems and other recovery or maintenance tools commonly used for troubleshooting computers.

One of the included features of Rufus is the ability to download official Windows ISO images directly from Microsoft servers. This allows users to obtain original installation images for Windows 8.1, Windows 10, and Windows 11 without searching for them on third-party websites.

In addition to creating bootable drives, Rufus can format USB devices. It supports several file systems including FAT32, NTFS, exFAT, UDF, and ReFS. This flexibility allows the USB drive to be prepared for different use cases and compatibility requirements.